This article is a review of the studies:

Varshney, A.K., Srimathi, T., Singh, A., Gaurav, R., Pandit, A., Lodha, D.H. Investor Herding Behaviour During Financial Crises: A Comparative Study. Advances in Consumer Research, 2025. https://acr-journal.com/article/investor-herding-behaviour-during-financial-crises-a-comparative-study-1560/?utm_source=chatgpt.com

Wang, H. Event-Driven Market Co-Movement Dynamics in Critical Mineral Equities: An Empirical Framework Using Change Point Detection and Cross-Sectional Analysis. 2026. https://doi.org/10.48550/arXiv.2601.10851

Crises are traditionally examined through the lens of macroeconomic shocks, including declining liquidity, rising inflation, reduced economic activity, and deteriorating expectations among businesses and consumers. Their consequences extend beyond the real sector, as instability is directly transmitted to financial markets, amplifying volatility and reshaping the behavior of market participants.

Contemporary research in finance suggests that during such periods, not only fundamental economic indicators but also investor behavior becomes critically important. As uncertainty intensifies, investors increasingly base their decisions not solely on fundamental and technical analysis, but also on fear, informational noise, and the actions of the majority. This, in turn, has direct implications for the effectiveness of diversification.

According to classical financial theory, allocating capital across a range of assets should reduce the overall risk of a portfolio. In practice, however, crisis periods often reveal the opposite effect: asset prices begin to move more synchronously, correlations increase, and the protective capacity of diversification weakens precisely when it is most needed.

This issue is explored in two recent studies: the analysis of investor herding behavior during financial crises (Varshney et al., 2025) and the examination of asset co-movement in the critical minerals sector (Wang, 2026). The findings highlight the growing importance of behavioral factors, including their role in shaping the effectiveness of diversification.

Further insight into these conclusions can be gained by comparing them with the practices of sovereign wealth fund management, where variations in returns across different periods illustrate how distinct asset allocation strategies perform under conditions of market stress.

One of the key mechanisms behind the weakening of diversification during crises is herding behavior. It emerges when investors begin to replicate the actions of the majority, even when such behavior does not fully align with their own information sets or investment strategies.

The study by Varshney et al. (2025), based on data from the Indian stock market, examines herding behavior using the approach developed by Christie and Huang (1995), which relies on analyzing the dispersion of individual asset returns relative to the market index. The authors employ two primary statistical measures:

The findings indicate that during crisis periods, dispersion metrics decline despite an overall increase in market turbulence. This is interpreted as evidence that investors cease to act independently and instead move in line with the broader market. In the Indian stock market over the period 2019-2021, investors were more likely to follow general market trends rather than rely on independent asset evaluation. Moreover, signs of collective behavior persisted even after the most acute phase of the crisis had passed.

This insight is critical for understanding the limitations of diversification. During crises, as investor behavior becomes more homogeneous, asset price movements grow increasingly synchronized, and cross-asset differences diminish. As a result, the effectiveness of diversification as a risk management tool declines, and even a well-balanced portfolio may fail to ensure positive returns.

Additional insight is provided by the study of Wang (2026), which examines asset co-movement within the critical minerals sector. The author employs the Change Point Detection (CPD) methodology, a technique used to identify structural breaks in time series data. Using the PELT (Pruned Exact Linear Time) algorithm, the study detects points at which the statistical properties of the market change significantly following major events, including:

After identifying these structural breakpoints, the study analyzes CSSD and CSAD indicators to assess the degree of collective investor behavior. The results demonstrate that following major market shocks, assets within the examined sector tend to move in a significantly more synchronized manner.

The increase in asset co-movement reflects a rise in return correlations. Under such conditions, even a diversified portfolio composed of different asset classes loses part of its protective capacity, as assets begin to respond similarly to common macroeconomic and informational shocks.

At the same time, the nature of the crisis plays a crucial role. Systemic shocks tend to intensify herding behavior and compress cross-asset differences. In contrast, more localized geopolitical events may restore differentiation: investors engage in more selective risk assessment, and asset behavior becomes more heterogeneous once again.

A particularly valuable perspective on the effectiveness of diversification during crisis periods can be gained from comparing the practices of sovereign wealth fund management. Unlike private investment portfolios, sovereign funds implement long-term institutional strategies aimed not only at generating returns but also at ensuring macroeconomic stability. As a result, behavioral factors are minimized in their investment decision-making processes.

Nevertheless, return dynamics indicate that herd behavior in financial markets, typically associated with individual investors, can also negatively influence the performance of large institutional investors.

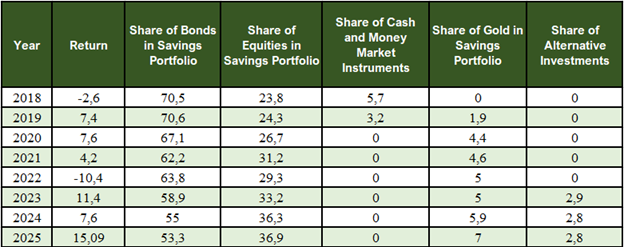

The National Fund of the Republic of Kazakhstan demonstrates, over the observed period, a transition from a predominantly conservative asset allocation model toward a more balanced structure of its savings portfolio.

Data presented in Table 1 indicate a gradual shift in asset allocation between 2018 and 2025. The most notable trend is the decline in the share of bonds within the portfolio, decreasing from 70.5% in 2018 to 53.3% in 2025. Since bonds traditionally serve the function of reducing volatility and protecting capital, this change indicates a gradual increase in the fund's willingness to accept higher market risk in order to increase potential returns.

At the same time, an increase in the share of equities can be observed. While equities accounted for 23.8% of the portfolio in 2018, their share rose to 36.9% by 2025. A higher allocation to equities reflects a stronger orientation toward long-term asset value growth and more active participation in global market dynamics.

Another significant development was the inclusion of gold in the structure of the savings portfolio. In 2018, this asset was absent, whereas by 2025 its share had reached 7.0%. From a risk management perspective, this is particularly important, as gold is traditionally regarded as a safe-haven asset during periods of heightened uncertainty, inflationary pressure, and financial instability.

An additional dimension of diversification was introduced through alternative investments. While such instruments were not present at the beginning of the observed period, their share reached 2.8% by 2025.

Overall, the structure of the National Fund of Kazakhstan reflects a transition from a model primarily focused on capital preservation to a more complex system of risk allocation across multiple asset classes.

At the same time, return indicators demonstrate that diversification does not provide complete protection for large institutional investors. During the 2022 shock, for instance, the fund recorded a return of (-)10.4%. Even a substantial share of defensive instruments was insufficient to fully offset the impact of global financial tightening, rising interest rates, and geopolitical instability.

The Government Pension Fund Global of Norway represents an alternative model of sovereign wealth management, characterized from the outset by a higher degree of diversification and a greater tolerance for market volatility.

According to the data presented in Table 2, the structure of the Norwegian fund has remained consistently oriented toward higher-risk assets throughout the observed period. The share of equities has remained stable at around 70%, reaching 71.3% in 2025. This is significantly higher than the corresponding figure for the National Fund of Kazakhstan. A high allocation to equities allows the fund to benefit more strongly from periods of global market growth, but it also increases its sensitivity to crisis-driven market downturns. The share of bonds in the Norwegian fund is considerably lower, fluctuating within the range of 26-30%, indicating a less pronounced defensive component within the portfolio.

Additional diversification is achieved through investments in real estate and renewable energy infrastructure. Although these asset classes constitute a relatively small share of the portfolio, they broaden the sources of return and reduce dependence on public financial markets alone.

The financial performance of the Norwegian fund reflects the higher volatility of its strategy. In the crisis year of 2022, the fund recorded a return of (-)14.1%, which was lower than that of the National Fund of Kazakhstan. This confirms the greater sensitivity of a risk-oriented portfolio to global market shocks. However, during periods of recovery and growth in global markets, such a strategy delivers stronger performance.

A comparison of the two sovereign wealth funds, the National Fund of the Republic of Kazakhstan and the Government Pension Fund Global, clearly demonstrates that during crisis periods, despite differences in the degree and structure of diversification, both funds experience negative returns. This indicates that even a well-diversified portfolio cannot fully avoid drawdowns in periods of systemic shocks, when asset co-movement intensifies and the effectiveness of diversification declines.

At the same time, the experience of sovereign funds reveals a fundamental trade-off between stability and return within investment strategy.

The model of the Kazakh fund is primarily oriented toward capital preservation and is characterized by a more conservative asset structure. A significant allocation to bonds, along with the inclusion of gold, helps reduce the depth of drawdowns during periods of market stress. Such a strategy provides relative portfolio stability but limits long-term return potential.

In contrast, the Norwegian fund model reflects a deliberate acceptance of higher short-term volatility in exchange for stronger long-term returns. A substantial allocation to equities makes the fund more sensitive to different phases of the market cycle, while simultaneously enabling a higher growth potential during favorable market conditions.

By integrating insights from academic research and the practical experience of sovereign wealth funds, several key conclusions can be drawn:

Contemporary research confirms that financial crises amplify the role of behavioral factors and make markets more sensitive to collective investor psychology. Herding behavior and the increasing co-movement of assets weaken the classical benefits of diversification during periods of stress.

Therefore, the key challenge for investors is not merely the implementation of diversification, but the selection of a portfolio structure that aligns with their investment horizon, tolerance for drawdowns, and ability to maintain discipline during periods of market instability.